Open Banking Britain represents a fundamental structural shift in how the United Kingdom’s financial architecture operates, moving away from closed, proprietary data silos toward a more interconnected and transparent ecosystem. While much of the initial public discourse focused on consumer-facing applications, the most significant impact is currently being felt in the back offices of British businesses, where cash flow management and payment processing are undergoing a silent, yet total, transformation. By granting authorized third-party providers access to financial data through secure Application Programming Interfaces, firms can now achieve a level of granular visibility that was previously reserved for the largest financial institutions with massive proprietary IT budgets.

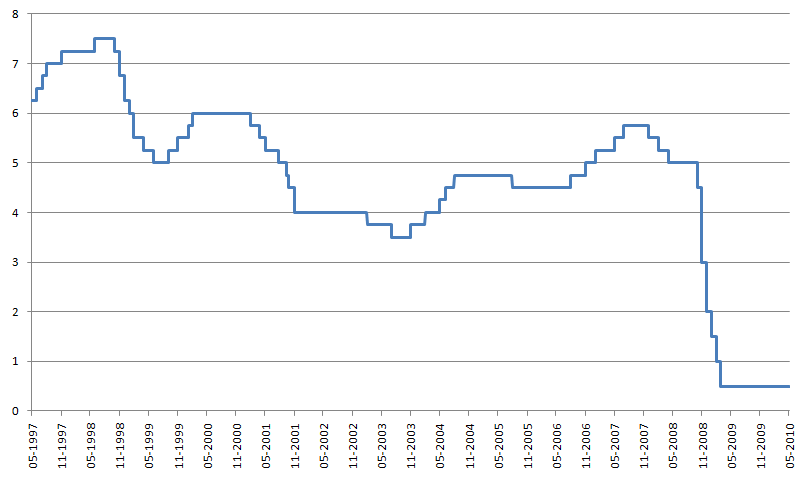

The core philosophy of this framework lies in the democratization of financial data, which serves to lower the barriers to entry for smaller enterprises attempting to optimize their liquidity. When a firm can plug its accounting software directly into its bank accounts, the latency between a transaction occurring and that data appearing in the ledger effectively vanishes. This integration allows for real-time reconciliation, which is essential for businesses navigating volatile economic climates. As market dynamics fluctuate, understanding the nuances of Bank of England interest rates becomes much simpler when one has an immediate, accurate view of current cash positions and future projections.

The Structural Evolution of Open Banking Britain

Open Banking Britain has matured from a regulatory obligation imposed on the big banks into a strategic asset for the private sector, forcing a rethinking of commercial banking relationships. For decades, the high street banks held a monopoly over account data, creating a friction-heavy environment where switching costs were prohibitively high and operational integration was cumbersome. Today, the ability to initiate payments directly from an accounting package, without the need for traditional card rails, offers an immediate reduction in transaction costs. This is not merely a technical efficiency gain; it is a competitive advantage that reshapes the internal cost structures of businesses, allowing them to reinvest capital that was previously trapped in high-fee payment processing channels.

Furthermore, the evolution of fintech startups has been intrinsically linked to this regulatory framework, as these entities have built their entire business models around the fluidity of data. These startups are not simply mimicking traditional banking services but are creating entirely new categories of treasury management software. By leveraging the standardised protocols developed under this regime, they provide small and medium-sized enterprises with sophisticated cash-flow forecasting tools that were historically restricted to corporate treasurers in multinational conglomerates. The result is a more resilient private sector that can anticipate funding gaps and manage working capital with an unprecedented degree of precision.

Strategic Implications for Corporate Finance

Corporate financial strategy is no longer limited to the data provided within quarterly statements or delayed bank reports, as the ongoing expansion of the digital economy allows for continuous, data-driven decision making. The integration of Open Banking Britain protocols into enterprise resource planning systems enables finance directors to monitor multiple accounts held at various institutions simultaneously, creating a centralized dashboard for holistic balance sheet management. This degree of oversight is particularly critical when companies are involved in high-stakes corporate actions or rapid expansion, where the speed of information often determines the feasibility of a successful outcome. In an era where private equity firms are increasingly monitoring companies for potential acquisition, maintaining a clean, digitized, and transparent financial record is paramount.

The transition is not without its operational risks, particularly regarding cybersecurity and data privacy, which remain top-of-mind for those overseeing the implementation of these protocols. Banks and fintech partners have had to invest heavily in robust API security to ensure that the increased flow of sensitive commercial data remains protected from unauthorized interception. Despite these challenges, the trajectory of adoption is clear; firms that fail to integrate these tools into their daily operations will find themselves at a distinct disadvantage compared to rivals that can execute payments and reconcile accounts in seconds rather than days. As global markets look toward the digital economy as a primary driver of growth, the UK’s experience serves as a case study in how regulatory policy can catalyze private sector innovation.

Looking Toward a Connected Financial Future

Looking ahead, the next phase of this financial evolution will likely involve the expansion into open finance, where the principles applied to banking are extended to investment, insurance, and pension data. This integration will create a comprehensive view of a company’s financial footprint, enabling more nuanced lending decisions by financial institutions that can finally assess risk based on real-time behavior rather than static, historical records. For the average British business owner, this means that credit will become more accessible and, crucially, better priced to reflect actual operational risk. The ability to pull live data into loan applications effectively removes the information asymmetry that has historically hindered smaller firms from accessing the capital markets.

In conclusion, while the initial rollout of these data-sharing mandates was met with skepticism and logistical friction, the long-term benefits are now manifesting as a core pillar of British commercial efficiency. We are moving away from the era of periodic reporting toward a system of permanent, real-time financial transparency. Businesses that treat these changes as a regulatory hurdle to be cleared rather than an opportunity to be exploited will miss the shift in the commercial landscape. The true value lies in the data, and in the ability to turn that data into actionable intelligence that drives sustainable, long-term growth across the United Kingdom.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}